.png)

Delta Vega introduces the Structured Product Risk Score (SPRS), an innovative risk metric capturing the complex risk exposure induced by structured products and converting it into a simple and intuitive score.

From Structured Product to SPRS

Structured products are diverse in their underlying assets (indices, basket of stocks, individual stocks, etc.), payoffs and embedded options. The SPRS is the risk compass that will help investors navigate in the universe of structured products investment opportunities.

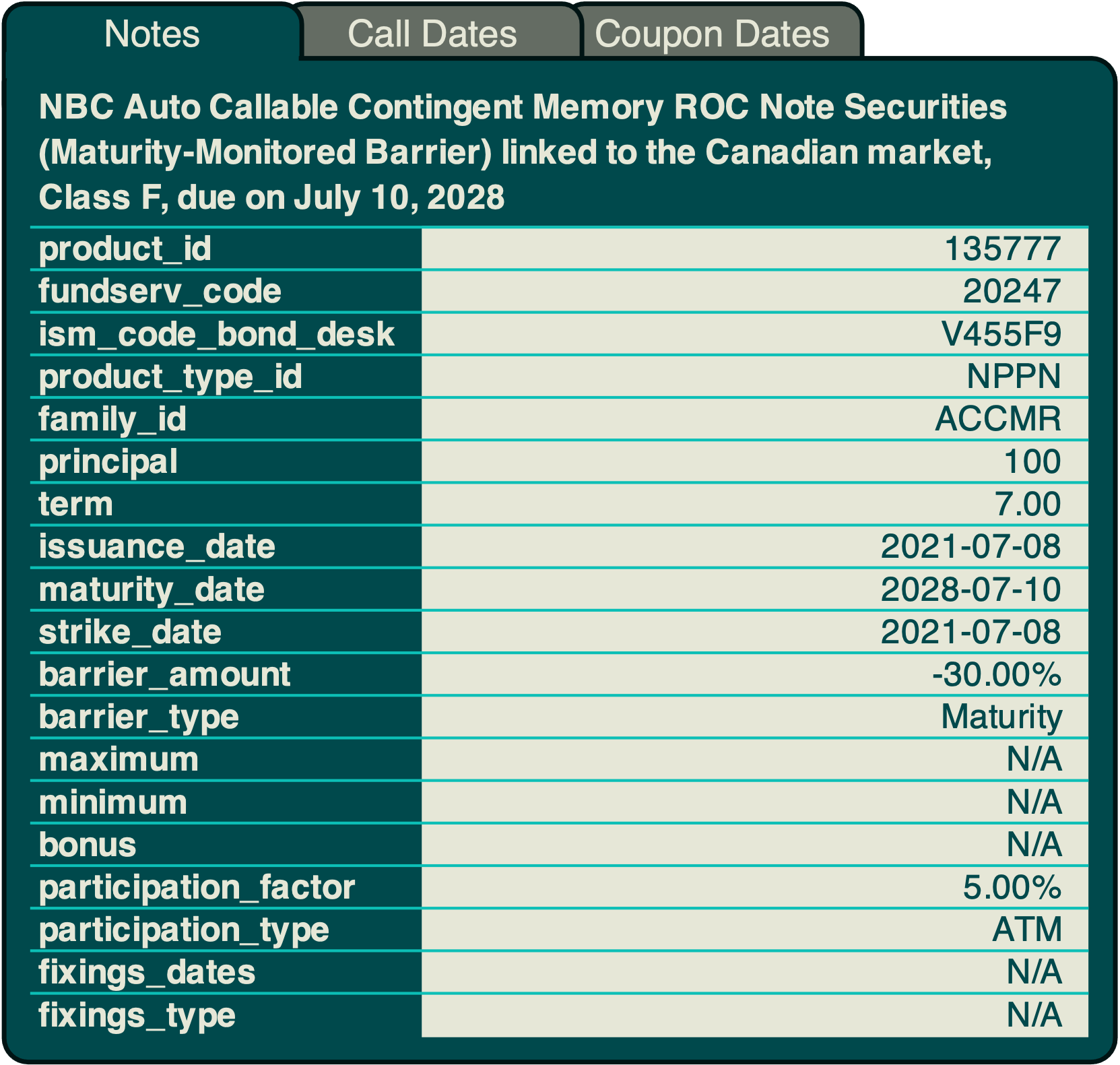

A structured product is fully described by its contract features

Know Exactly What You Own

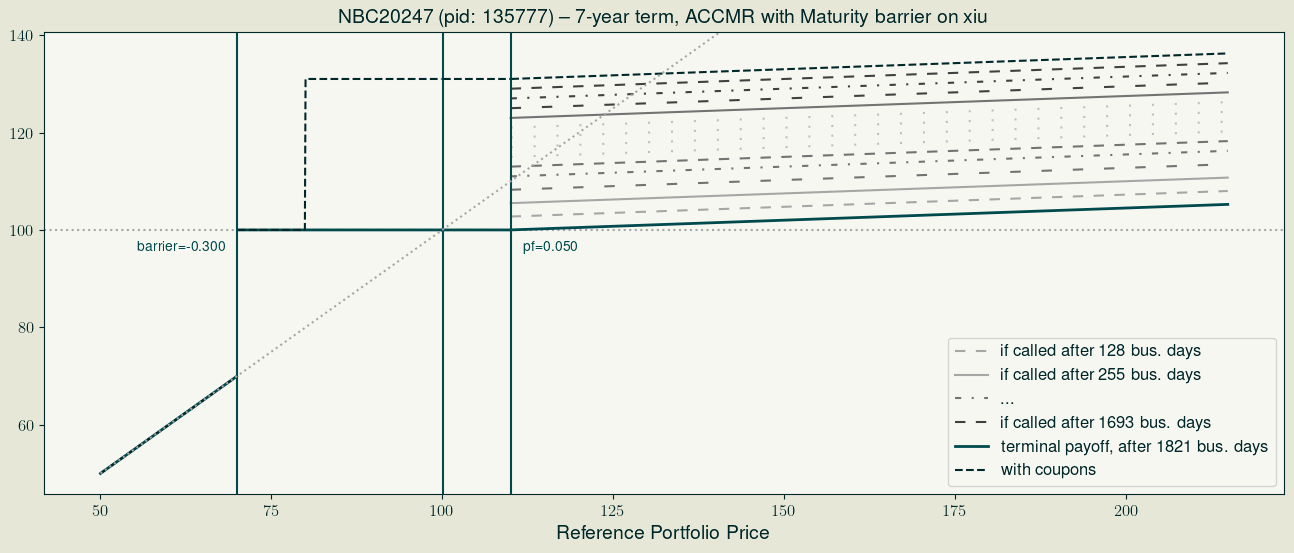

Our analytics engine converts these features into a mathematical representation of the product. This formulation allows mapping any possible sequence of future returns on the reference portfolio to its corresponding payoff.

The payoff diagram below represents only a fraction of the scenarios for the terminal value of the structured product in the above example as a function of the reference portfolio price return:

Between the capital protection, the conditional coupons and the potential call dates, projecting various scenarios on a single graph illustrates the complexity of the payoff structure. This complexity limits the scope of most traditional risk measures. Our score summarizes the potential downside risk at any given point in time. In particular, it evolves with:

Current market conditions, e.g. endogenizing sudden market turmoil,

Resolved uncertainty regarding cash flows, e.g. paid coupons and how (un)likely the product is to be called,

Riskiness relative to an investment in a well-diversified portfolio, e.g., a capital-protected note’s absolute riskiness might increase given market conditions, but less so than that of a benchmark portfolio lacking that capital protection.

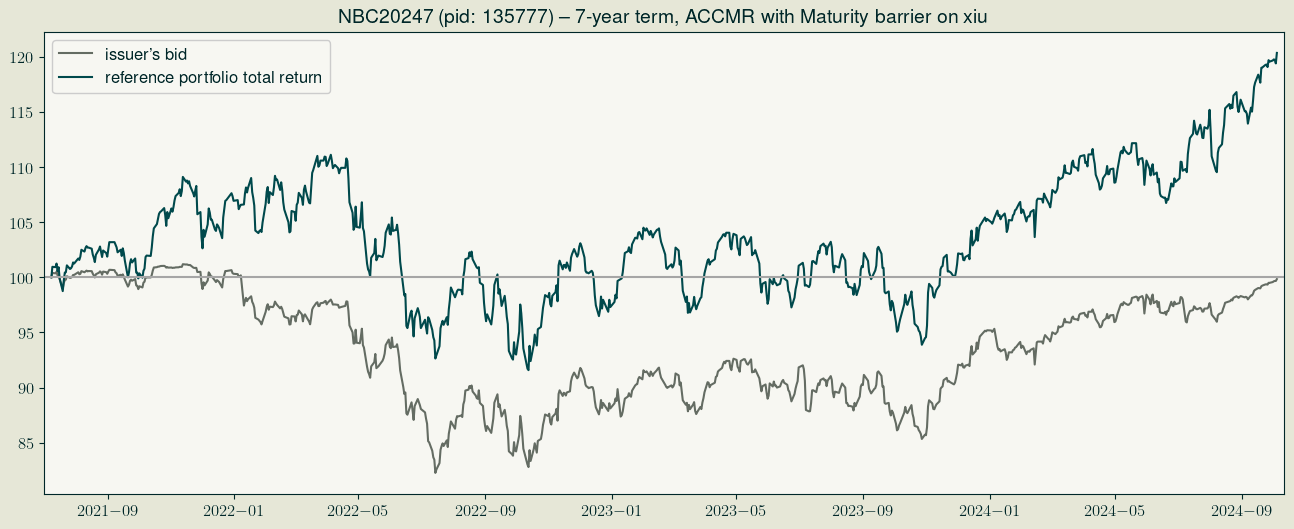

Measure Risk as It Evolves

At each point in time, the reference portfolio total return and the bid price of the structured product’s issuer are collected (basis = 100 at issuance), along with several other market indicators:

Accounting for the current market conditions, Delta Vega estimates a valuation model on the underlying asset price. The model incorporates state-of-the-art financial modelling tools including stochastic volatility, time-varying risk premia for market, and firm-specific risk factors.

Once the model is estimated, scenarios for the underlying asset price are generated by means of a filtered historical simulation – a technique well suited to capture the structured products’ non-linearities and their exposure to tail risk.

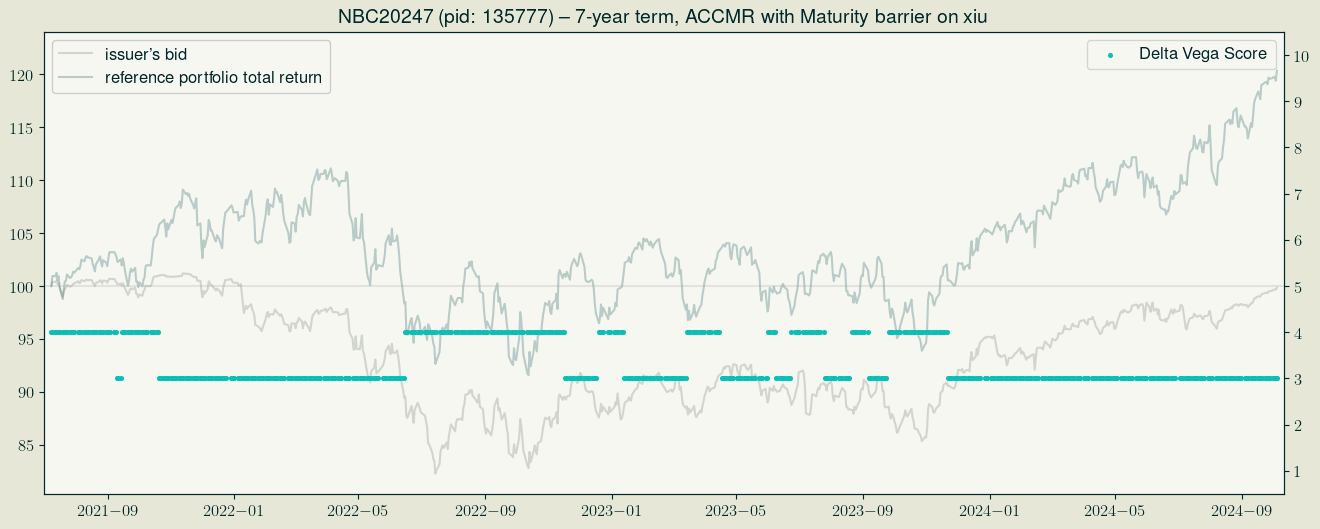

One Score. Instant Clarity.

The Score is then calculated on a 1 (safest) to 10 (riskiest) scale, based on the shape of the distribution of losses.

The SPRS allows the investor to benchmark the risk exposure of the structured product: to a passive investment strategy (5 is the score for investing in the iShares S&P/TSX 60 Index ETF, ticker: XIU), to a direct investment in the underlying asset.

In conclusion, the granular scale of the SPRS facilitates cross-products comparisons. The frequent updating of the SPRS allows investors to make timely, well-informed decisions, and issuers to better document their risk management. Its adoption will lead the industry to an enhanced standardization beneficial to all industry stakeholders.

Integrating The Structured Product Risk Score

Contactof your work

structured products

reach its goal